12 Jun 2024

12 Jun 2024

Key market indicators portray a relatively buoyant and dynamic market under the strain of a growing supply-demand imbalance, according to Home.co.uk's Asking Price Index for June.

However, oversupply concerns persist. Despite greater market optimism, spurred by improving inflation figures and therefore expectations of a rate cut, demand is looking outpaced.

Vast amounts of properties continue to move through the current UK sales market; aside from three busy months last year, this is a level of activity not seen since the final quarter of 2018, but sales stock levels continue to swell.

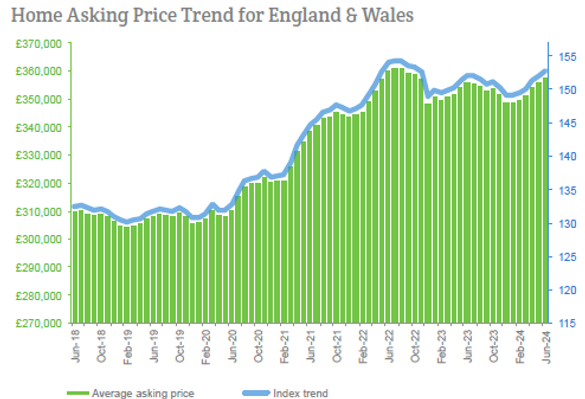

The mix-adjusted average asking price increased by 0.5% during the last month but prices remain essentially on a par with last summer overall and have yet to return to their 2022 high.

Notably, the northern regions are indicating significant positive annualised growth while poorer performing regions such as the East of England and the South West remain significantly down compared to June 2023.

This mixed picture of regional market performance, with the North consistently outperforming the South post- COVID, looks set to persist while yields in the northern regions offer considerably better returns to investors.

A cut in the Bank of England base rate is both justifiable, thanks to lower inflation, and necessary to shore up the weaker regional markets.

But Rishi Sunak's decision to call a general election on the 4th of July means the City now expects action later in the summer or even early autumn, after the voting is over. Already, the sloth-like inaction of the Bank has put the UK economy at a disadvantage compared to European countries where rates have already begun to come down.

In view of the plentiful supply of properties for sale and the inevitable election disruption, the potential for further price growth appears rather limited over the coming months. More likely is that prices will go sideways until borrowing costs finally come down and boost demand.

Price cutting of properties currently on the market remains within the normal range; in fact, the total of reduced properties is very similar to that observed during the summer months of 2019. Hence, for the time being, most vendors remain hopeful, even in the slower regional markets, but this situation could change rapidly as patience wears thin.

Whilst the Typical Time on Market has increased in all regions except London compared to June 2023, the same median time on market figures remain much improved in most regions compared to June 2019. Therefore, whilst slower than last year, properties continue to move through the market at a fairly normal pace, relative to previous observations.

Asking rents continue to show positive, albeit lower, growth in all regions except Greater London and the West Midlands (-1.7% and -1.0% respectively). Scotland, Yorkshire and the North East still boast double-digit annualised growth. UK asking rents are currently 3.0% above their May 2023 reading.

The annualised mix-adjusted average asking price growth (sales) across England and Wales is now 0.5%; in June 2023, the annualised rate of increase of home prices was still negative at -1.3%.

Headlines

- Asking prices have risen 0.5% since last month across England and Wales (the fifth consecutive monthly rise) and are up just 0.5% compared to June 2023.

- The total unsold sales stock count for England and Wales increased again during the last month. Nearly 10,000 properties were added to agents' portfolios, making the current count of 485,269 the highest June total since 2014.

- Prices increased again in all English regions, Wales and Scotland during the last month. Vendors in the East of England were the least optimistic and upped their asking prices by the smallest margin (0.1%), while vendors in Yorkshire and the West Midlands were the most bullish, raising their prices by a full percentage point.

- Despite the vast amount of stock for sale, market momentum remains relatively healthy as shown by the Typical Time on Market (median) for unsold property in England and Wales being seven days less than in June 2019. However, the current median is four days more than in June last year.

- The total number of new instructions entering the market during May 2024 was 14% more than during May 2023. However, the total is 2% less than in May 2019.

- The North West remains the regional property market growth leader with a year-on-year gain of 3.8%, while the East of England is now the worst performing region with a loss of -1.5% over the same period.

- The annualised national growth figure for asking rents has slowed to just 3.0%. However, the North East and Yorkshire continue to lead the regional growth table, indicating rises of 15% and 16% respectively year-on-year. Meanwhile, the decline in Greater London rents has slowed to -1.7%.

- Prime central London rents have recovered some of their lost ground over recent months. For instance, Kensington and Chelsea rents have rebounded 13% over the last quarter but remain down year-on-year by 10%.

For media enquiries please contact: press@home.co.uk 0845 373 3580

For more information visit here.

Follow us on X.