12 Jul 2024

12 Jul 2024

Overall home price rises are being kept in check by high stock levels and stubbornly high mortgage costs, according to Home.co.uk's asking price index for July.

But there is regional variation. While Greater London, adjacent regions and the South West remain in recovery mode, the northern, Scottish and Welsh markets have more than made up for lost ground following the shock price drop in December 2022 and continue to thrive.

Key market indicators show that, despite lacklustre performances in the southern markets, the UK property market is in much better shape overall than in 2019.

This is clearly remarkable and perhaps counterintuitive given the current higher levels of stock for sale and substantially higher borrowing costs.

However, during the same 5-year period, UK rents have risen by 44.6% and this meteoric rise has provided enormous support for the sales market. Moreover, this support has a regional bias with respect to gross rental yields which are higher in the North.

Clearly, without this vast support from the rental market, the sales market would be in a much worse state. Keir Starmer's new government needs to understand that rent fundamentally underpins the value of property and therefore future legislation regarding the lettings market should be very carefully considered.

Indeed, activists' calls for rent controls and an end to contractual tenure casts dark shadows over the future of both the sales and rental markets.

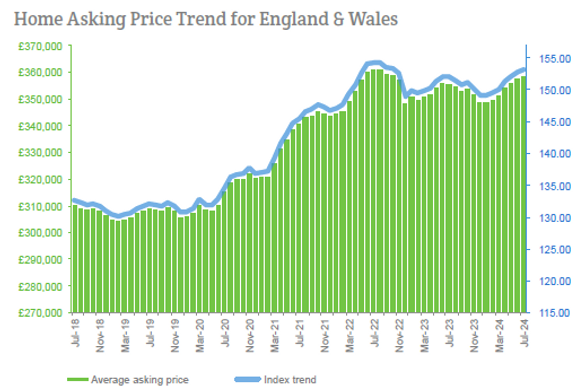

The mix-adjusted average asking price for England and Wales increased by a muted 0.2% during the last month and, while a little above the high of last summer, remains below the highs of 2022.

Given that inflation has fallen below target, a cut in the Bank of England base rate is becoming long overdue. The Bank's reasoning for persisting with high rates to curb wage growth seems both cruel and cynical, given that remuneration is merely catching up with the cost-of-living rise that the same institution created.

Meanwhile, the wider UK economy continues to suffer while European competitors already benefit from the first rate cuts. Investment in much-needed new-builds is also being thwarted by unnecessarily high interest rates. In particular, additional new energy-efficient rental stock is required to ease the shortfall of properties available to let. In July 2019, 122,000 properties were available for rent while today the total is 66,000.

Despite buyers' frustration with borrowing costs, vendors remain patient. In fact, price-cutting of properties while on the market declined between May and June, in terms of both the number of properties and the average discount.

Indeed, Typical Time on Market remains very reasonable given the higher stock levels; it is slightly slower than last year when stock was limited but considerably better than in July 2019.

Asking rents continue to show positive, albeit lower, growth in most regions although year-on year falls are evident in Greater London, East Midlands and the West Midlands (-1.2%, -0.6% and -0.5% respectively). Scotland, Wales, Yorkshire, the South West and the North East indicate double-digit annualised growth.

UK asking rents are currently 2.5% above their July 2023 reading.

The annualised mix-adjusted average asking price growth (sales) across England and Wales is now 0.7%; in July 2023, the annualised growth of home prices was in the red at -1.5%.

Headlines

- Asking prices nudged up 0.2% during the last month across England and Wales (the sixth consecutive monthly rise) and are now up 0.7% compared to July 2023.

- The unsold sales stock count for England and Wales increased again during the last month to reach a 10-year high for July. Nearly 4,000 properties were added to agents' portfolios, making the current total 489,086.

- Prices increased again in all English regions (except the North West) and Wales during the last month. The mix-adjusted average was trimmed by 0.5% in Scotland and by 0.2% in the North West. Prices remained unchanged in the South West. Vendors in the North East were the most bullish, raising their prices by 0.9%.

- Despite the relatively large amount of stock for sale, market momentum remains relatively healthy as indicated by both the Typical Time on Market (median) for unsold property being seven days less than in July 2019 and our Market Turnover Indicator. However, the current median time on market for unsold property in England and Wales is six days more than in July last year.

- The total number of new instructions entering the market during June 2024 was 4% more than during June 2023.

- The North East is the new regional property market growth leader with a year-on-year gain of 4.8%, while the South West is now the worst performing region with a loss of -1.2% over the same period.

- The annualised national growth figure for asking rents has slowed further to just 2.5%. However, the North East and Wales continue to lead the regional growth table, indicating rises of 14.5% and 12.8% respectively year-on-year. Meanwhile, the decline in Greater London rents has slowed to -1.2%.

- The London boroughs of Redbridge and Havering are the current growth leaders with annualised rental growth of 13.0% and 10.1% respectively.

For media enquiries please contact: press@home.co.uk 0845 373 3580

For more information visit here.

Follow us on X.