13 Sep 2024

13 Sep 2024

A surge in new instructions has swelled estate agents' portfolios further, according to Home.co.uk's Asking Price Index for September.

However, given the large number of properties entering the market last month, the current total of stock for sale has only increased by a comparatively small margin. Hence, demand remains sufficiently strong to have prevented a large glut of unsold properties.

Vendors are clearly motivated given that, seasonally, prices usually dip from here towards the Christmas break. The drop in the bank rate will have been the green light for many vendors to commit, but a substantial and growing landlord exodus has also been observed.

Of course, higher stock levels put downward pressure on prices. The last time the total stock of unsold properties on the market was this high was in 2019 and that year prices essentially went sideways (despite the base rate being a mere 0.75%).

For the time being, it is reassuring that the rate at which properties are moving through the market is considerably higher than in 2019, although given the recent uptick in inflation (and the Bank of England's poor track record on forecasting), this may not be the case for much longer. Buyer optimism could evaporate very quickly should monetary inflation be found to be out of control again.

Overall, a two-speed market persists. The northern regions of England, the West Midlands, Scotland and Wales show all the indications of vibrant markets with price growth over and above inflation. The North East, in particular, is racing ahead and has shown very strong price growth over the last twelve months.

Elsewhere, prices have essentially stayed still this year and certainly have not yet recovered their 2022 highs.

The East of England and Greater London still have the most ground to make up before they return to the 2022 price highs.

Meanwhile, the East, South East and the South West still have a few percentage points to recover. Given the high stock levels in these regions, we expect further recovery to remain very slow. Indeed, a further rate cut may be needed to elicit significant price growth through greater demand.

Despite the poor prospects for price growth in some regions, the UK property market is operating within normal parameters and could step up a gear next year if borrowing costs continue their steady decline.

However, the risk of a further bout of inflation, tax increases and rent controls all continue to be dark clouds on the housing market horizon.

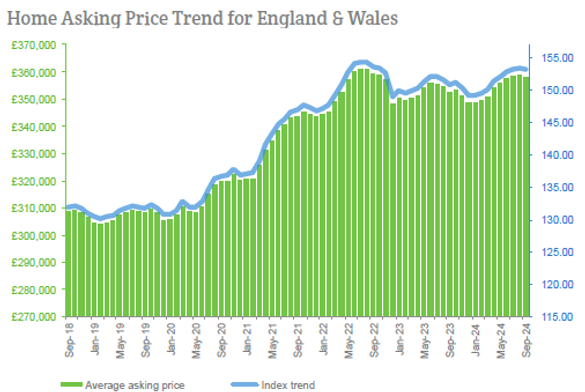

The annualised mix-adjusted average asking price growth (sales) across England and Wales is now 1.5%; in September 2023, the annualised growth of home prices was -1.8%.

Headlines

- Asking prices dipped for the first time in nine months, by 0.2%, during the last month across England and Wales, yielding to both high supply and seasonal trends. Home prices are up 1.5% compared to September 2023.

- The worst monthly falls were in London and the West Midlands while prices continue to increase in Scotland, the North West and North East.

- The total number of new instructions entering the market during August 2024 was 14% more than during August 2023 and 8% more than August 2019.

- The unsold sales stock count for England and Wales increased again to make the current total the highest since November 2014. Nearly five thousand properties were added to agents' portfolios, making the current count of unsold properties 499,667.

- Despite both a notable slowdown and a 10-year high in unsold stock, the sales market momentum remains relatively healthy, as indicated by both the Typical Time on Market (median) for unsold property in England and Wales being seven days less than in September 2019 and our Market Turnover Indicator showing a performance comparable to pre-pandemic years. The current median Time on Market for unsold property is five days more than in August last year.

- The North East extends its lead as the regional property market growth leader with a very impressive year-on-year gain of 6.7%, while the East of England is now the worst performing region, indicating no change over the same period.

- The annualised national growth figure for asking rents has slowed again to just 0.8%, dragged down by London's poor performance. However, Wales continues to lead the regional growth table, followed by the South West, indicating rises of 14.6% and 9.7% respectively year-on-year. Meanwhile, the year-on-year decline in Greater London rents is now -1.1%.

- The boroughs of Haringey and Bexley indicate the worst declines in asking rents, with annualised rental falls of 10.7% and 8.9% respectively.

For more information visit here.

For media enquiries please contact: press@home.co.uk 0845 373 3580

Visit us on X.