17 Oct 2024

17 Oct 2024

An autumn surge in home prices reflects a rise in confidence amongst vendors and the market overall, according to Home.co.uk's Asking Price Index for October.

Such optimism has been fuelled by expectations of gradual interest rate cuts over the coming months.

The same optimism has encouraged many potential vendors to commit, resulting in a ten-year high in sales listings.

Landlords downsizing their portfolios, particularly in London, has also contributed to this record number of listings. However, this is leaving renters facing a chronic lack of supply.

While the number of properties available to let has increased by 25% since October last year, the total remains 21% lower than in October 2019, Home.co.uk found.

Landlords clearly need more incentives (and assurances) to stay in the market and increase the supply of essential quality housing. Until this is achieved, renters will continue to suffer high rents and lack of choice.

Despite above average supply, the sales market is attracting sufficient demand to keep marketing times low and property turnover high. The wait-and-see period following the Truss-Kwarteng debacle appears to be over. Significant pent-up demand has been unleashed on the market over recent months due to the more favourable interest rate outlook. However, whether inflation is now truly under control remains to be seen.

At the regional level, the market is highly diverse in terms of price growth.

The northern regions of England, the West Midlands, Scotland and Wales continue to show consistent strength with growth over and above inflation. The North East, in particular, continues to impress with spectacular price growth over the last twelve months. Elsewhere, nominal prices have essentially stagnated this year and lost ground in real terms.

The East and the South West are the poorest performers over the last twelve months in terms of price growth. Asking prices increased a mere 0.4% in both regions, indicating that a price correction is still ongoing in these markets in real terms.

The South West shows the highest increase in Typical Time on Market of unsold property since October last year due to reduced demand.

Despite these sluggish regions, the overall UK property market is operating normally compared to pre-COVID years. Moreover, the sales market may well pick up the pace early next year should borrowing costs continue their steady decline, although this is far from certain as evidenced by a recent small rise in two-year swap rates.

Additionally, Rachel Reeves' first Labour Budget of the new Parliament will likely affect sentiment significantly.

Overall, UK asking rent growth has slowed to zero, although this annualised national growth figure obscures the vast regional disparities between Greater London at -3.6% and the two best performers, Wales (+15.1%) and the North East (+12.0%).

Given that London rents increased by 32% over the last five years, we are now observing a market pricing correction that may persist well into next year.

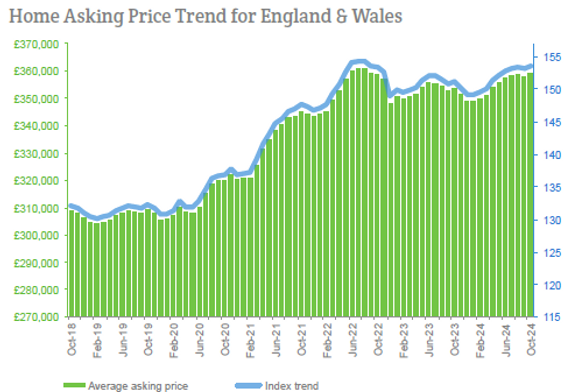

The annualised mix-adjusted average asking price growth (sales) across England and Wales is now 1.7%; in October 2023, the annualised growth of home prices was -1.5%.

Headlines

- Asking prices increased by 0.3% during the last month across England and Wales, supported by growing market confidence. Home prices are up 1.7% compared to October 2023.

- After two years of cautious recovery, the mix-adjusted average is now higher than in October 2022 but has yet to return to the peak of July 2022.

- Prices show month-on-month increases in Scotland, Wales and all English regions with the exception of the North East where the average remains unchanged.

- The total number of new instructions entering the market during September 2024 was 4% more than during September 2023 and 12% more than September 2019.

- The unsold sales stock count for England and Wales increased again to make the current total the highest since November 2014. Nearly 9,000 properties were added to agents' portfolios, making the current count of unsold properties 508,833.

- Despite the ten-year high in unsold stock, the sales market momentum remains relatively healthy as indicated by the Typical Time on Market (median) for unsold property in England and Wales being five days less than in October 2019. However, the current median time on market for unsold property is four days more than in October last year due to high inventory levels.

- The North East maintains its position as the regional property market growth leader by a large margin. The year-on-year gain remains at 6.7%, while the next best is Yorkshire at 3.7%.

- The East of England and the South West are the worst performing regions, with both indicating an increase of just 0.4% over the same period.

- The annualised national growth for asking rents has stalled (0.0%) when London's losses are included. However, Wales followed by the North East continue to indicate double-digit growth of 15.1% and 12.0% respectively year-on-year. Meanwhile, the year-on-year decline in Greater London rents is now -3.6%.

- The borough of Haringey shows the greatest decline in asking rents with an annualised rental fall of -14.0%.

For media enquiries please contact: press@home.co.uk 0845 373 3580

For more information visit here.

Follow us on X.