15 Jan 2025

15 Jan 2025

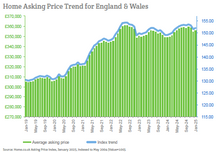

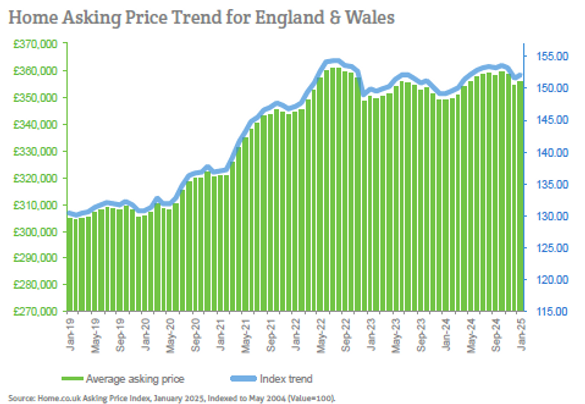

The UK property market begins the new year on a note of cautious optimism, according to Home.co.uk's Asking Price Index for January.

Prices are rising in line with seasonal expectations and buyer activity is picking up.

Increased supply attests to the fact that greater numbers of vendors are willing to commit, especially in London.

But whether demand will be able to match this level of supply is uncertain, especially after the increase in stamp duty from 1st April 2025.

With unsold stock levels at a nine-year high and supply still rising, there is a notable amount of downward pressure on prices.

However, regional differences are considerable, and we expect home prices in the North, Scotland and Wales to continue to outperform London and the South.

Market expectations are for a rate cut by the Bank of England in February and, should this materialise, buyer confidence may get the fillip it needs, at least in the short term.

For the time being, the vital signs of the UK property sales market indicate a positive state of health overall. The volume of property moving through the market is higher than during most of the five years prior to the pandemic.

Room for significant price growth appears limited due to both affordability constraints (the cost of borrowing and stamp duty) and increased supply.

The mix-adjusted average asking price for London and the southern regions remains lower, by a large margin, than the peak pricing observed in the summer months of 2022. Therefore, prices may not return to these levels in the lower performing regions in 2025.

UK asking rent growth remains sub-inflation at 1.5% overall. However, the national average is dragged down by Greater London at -1.9% while the best performers, East Midlands and Yorkshire, indicate 12.7% and 11.5% growth year-on-year respectively.

The annualised mix-adjusted average asking price growth (sales) across England and Wales is now 1.9%; in January 2024, the annualised growth of home prices was -0.5%.

Headlines

- Asking prices begin their seasonal ascent, rising 0.3% since last month across England and Wales. Annualised home price growth is now 1.9% overall.

- Seasonal price rises were observed in all English regions, while Scotland and Wales registered no change since last month. The largest rise was in London (0.7%).

- The UK property market continues to indicate significant momentum. Property turnover remains higher than during most of the last ten years and the Typical Time on Market is significantly lower than in pre-lockdown January 2020.

- The unsold sales stock count for England and Wales fell again during the last month, by around 9,000 properties. However, the current total of 456,216 is the largest such January figure since 2015.

- The total number of new instructions entering the market during December 2024 was 8% more than during December 2023. London saw the highest regional rise of 25%, a massive increase in supply.

- The North East retains its top position in regional property market growth, albeit with the year-on-year gain decreasing to 5.1%. In second place is Yorkshire at 4.6%.

- The East of England remains the worst performing region, indicating a tiny rise (0.4%) over the last twelve months.

- Overall, when taking inflation into account, the sales market has still yet to achieve real growth.

- The annualised national growth for asking rents is just 1.5% overall. This mix-adjusted average is affected disproportionately by London's rent falls (-1.2%). However, the East Midlands and Yorkshire indicate double-digit growth year-on-year.

- The City of London followed by Hackney indicate the largest declines in asking rents of all London boroughs, with annualised rental falls of 19.1% and 8.7% respectively. Meanwhile, rents in Kensington and Richmond are 10.9% and 6.8% higher than a year ago.

For media enquiries please contact: press@home.co.uk 0845 373 3580

For more information please visit

Follow us on X.