19 Feb 2025

19 Feb 2025

Sellers across Greater London and the South of England are resorting to competitive pricing due to high stock levels, according to Home.co.uk's February asking price index.

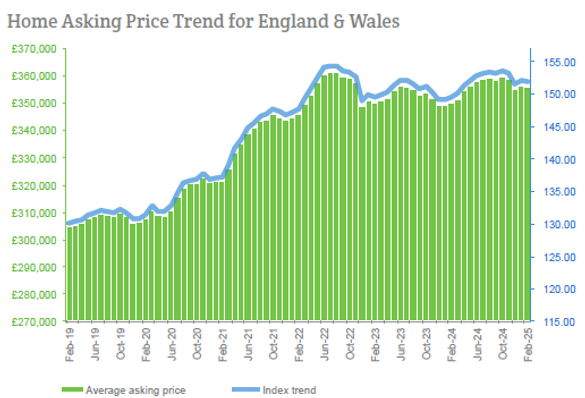

Contrary to seasonal expectations, the mix-adjusted national average asking price has dipped since last month, driven by significantly lower pricing in the capital as well as the South East and South West of England.

Even the Bank of England's cut in the base rate, which was arguably already priced into mortgage rates, was not enough to bolster confidence in a property market plagued by increasing taxation and regulation.

Consequently, vendors in these regions are increasingly willing to take a hit on their expectations to secure a sale.

In stark contrast, vendors in the North and Scotland are much more confident in their pricing. Among these top performing regions, Yorkshire indicated the largest monthly rise of 0.8%, seemingly a world apart from the pain felt in the South.

Undoubtedly, the relative performance of the Private Rented Sector (PRS) is a key factor in the North-South divide. Yields remain significantly better in the North and this factor does not look set to change soon.

In certain postal districts of London and the South East, rental yields are less than 3%; certainly not enough to pay a significant mortgage and all the other associated expenses.

Meanwhile, savvy investors can find yields as high as 12% in certain postal districts, all of which are to be found in the North.

These are the key factors driving the current market. Oversupply stems largely from landlords deciding to quit in low-yielding areas. Vendors and agents alike understand that demand is unlikely to be able to grow sufficiently to match the surge in new instructions, especially after the increase in stamp duty on April 1st.

The upside for savvy buyers is that there are certainly bargains to be had in some locations but, as many investors acknowledge, “catching a falling knife” is a risky business. The question that is difficult to answer is: When will the rate of supply return to more normal levels?

Since rental returns fundamentally underpin the value of property, the answer may well be: When yields return to a tenable level for investors. Logically, this would only be achieved through a combination of rising rents and falling prices.

Despite the difficulties in London and the South, the vital signs of the UK property sales market indicate a positive state of health overall, thanks to continued demand in the North. The current volume of property moving through the market is higher than in February last year, although the risk of a significant slowdown in London and the South is apparent.

The annualised mix-adjusted average asking price growth (sales) across England and Wales is now 1.7%; in February 2024, the annualised growth of home prices was -0.1%.

Headlines

- The expected seasonal rise in the national average asking price failed to materialise during the last month due to weaker pricing in London, the South East and the South West. Overall, asking prices have slipped by 0.1% since the January reading across England and Wales. Annualised home price growth is now just 1.7% overall.

- The total number of new instructions entering the market during January 2025 was 10% more than during January 2024. Oversupply is indicated in London and the South East which both show the highest regional increases, up by 21% and 13% respectively.

- Pricing remains strong in the North with Yorkshire and Scotland posting the largest month-on-month gains of 0.8% and 0.6% respectively.

- The North East cedes its top position in regional property market growth to Yorkshire which becomes the new leader with a year-on-year gain of 5.2%. Meanwhile, the South East replaces the East of England as the worst regional performer with an annualised gain of just 0.1%.

- For the time being, the UK property market continues to show significant momentum. Property turnover remains higher than the previous two February readings and the three February readings prior to the COVID event.

- The unsold sales stock count for England and Wales increased by around 13,000 properties during the last month, which is slightly above seasonal expectations. The current total of 469,279 is the largest February figure since 2013.

- Overall, price growth in the sales market continues to underperform relative to monetary inflation.

- At just 1.9%, annualised national growth in asking rents is also behind the rate of inflation. This mix-adjusted average is affected disproportionately by London's rent falls (-0.5%). However, the best performing region, the East Midlands, indicates 10.2% rental growth year-on-year.

- The City of London followed by Hounslow indicate the largest declines in asking rents of all London boroughs, with annualised rental falls of 18.9% and 7.7% respectively. Meanwhile, the best performers are Kingston-upon-Thames, Sutton and Wandsworth, with rents increasing by 8.9%, 8.8% and 8.3% respectively.

For media enquiries please contact: press@home.co.uk, 0845 373 3580

For more information visit here.

Follow us on X