15 Oct 2025

15 Oct 2025

Several issues are precipitating divestment from the UK property market, according to Home.co.uk's Asking Price Index for October.

As a result, agents' sales portfolios are bulging at the seams as investors attempt to cash out.

Higher interest rates, low or negative capital gains, increasing taxation, falling rents and adverse legislation are all factors in the decision-making process for landlords who are faced with a dilemma: do they hold on and hope or exit before the loss of earnings and control over their assets worsens?

However, the current market also presents a window of opportunity for both aspirant owner-occupiers and corporate landlords. For the bold, there are bargains to be had where pricing is weakest. Offers well below the asking price are more likely to be accepted in the current climate, although “catching a falling knife” is always a delicate affair.

For the time being, pricing is weakest in London, the South West, South East and the East of England. Moreover, this slow and painful price correction, in real terms, looks set to persist until confidence picks up again.

A cut in interest rates would certainly boost demand but, given persistent above-target inflation, this possibility looks unlikely in the near term.

Headlines

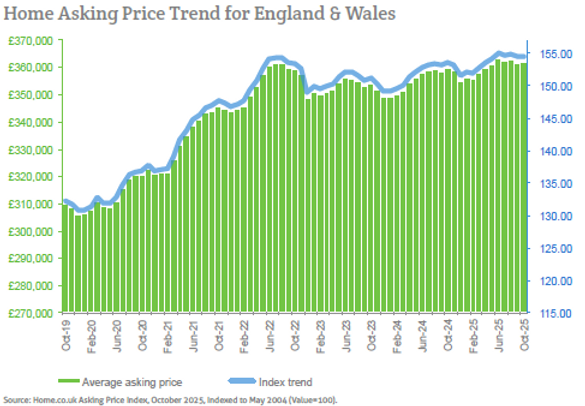

- The mix-adjusted average asking price for England and Wales edged up by the smallest of margins during September (0.1%), making the annualised growth figure a mere 0.6%. Scotland and the South West indicated the largest price falls.

- Annualised home price growth across England and Wales continues to be well below the level of inflation at just 0.6% overall. We estimate that overall real growth currently stands at around -4.4%. Even the best-performing regions are being outpaced by the current rate of inflation (RPI ex-housing).

- The unsold sales stock count for England and Wales is at its highest level since October 2013. Oversupply has created a buyer's market in most regions.

- Vendor hesitancy in an increasingly difficult market triggered a drop in supply of new sales properties during September. There were 11% fewer properties entering the market this year than in September 2024.

- Yorkshire is now the top regional property market growth leader with a year-on-year gain of 3.6%, overtaking the North West where growth has slipped to 3.1%. Meanwhile, the South West is now the worst regional performer with a painful annualised loss of 1.0%, narrowly outpacing London's annualised decline of 0.8%.

- Sales market momentum remains elevated compared to previous years. To date, this greater throughput has not been sufficient to significantly reduce the unsold stock total. Typical Time on Market for unsold properties is currently three days higher than in October last year and continues to trend higher.

- The annualised national growth in asking rents slides yet further into the negative (now -2.9%), driven down by a vast and unexpected increase in supply (27% year-on-year). The national growth figure is in the red due mainly to the negative performance of London, but negative contributions also now come from Scotland, Wales and all English regions except the North East.

- Only 13 of the 33 London boroughs indicate positive asking rent growth and five of those are below the 1% mark. In Bexley borough, albeit a relatively small rental market in the capital region, rents are down by 7.5% year-on-year.

For more information visit here.

For media enquiries please contact: press@home.co.uk 0845 373 3580

Follow us on X.