14 Nov 2025

14 Nov 2025

Oversupply in the UK property market is creating downward pressure on prices, Home.co.uk's House Price Index for November is warning.

Even the formerly top-performing northern regions are now showing sub-inflation growth. The key driver there was buy-to-let investment but, with negative capital gains in real terms and rents now sliding, investment impetus will inevitably wane.

The poor state of the wider economy is casting a long shadow. Rising unemployment and the expectation of tax rises in the November budget will erode the number of potential buyers and their buying potential. The market will therefore adjust to these new circumstances, most likely by reducing prices and rents.

The process will not be immediate. In fact, sub-inflation growth is already stealthily and gradually doing the job without triggering negative equity or distressed collateralised debt obligations (CDOs). Wiser investors realise the poor near-term prognosis for UK property, and some are indeed throwing in the towel.

As we head into the festive period, we can expect significant on-market reductions and more competitive pricing of new listings. Vendors can expect offers to come in below the asking price as buyers increasingly have the upper hand.

Regarding mortgage rates, there is some reason for optimism. A cut in the Bank of England base rate now appears to be priced in to the 2-year swap rate. This cut is expected to coincide with the MPC's December meeting where they will be dealing with the aftermath of Rachel Reeves' Autumn Budget, due to be released on November 26th.

The Chancellor has signalled that higher taxes on the wealthy will form part of the Autumn Budget package. Full details remain under discussion; officials have indicated that reforms to inheritance tax, capital gains tax, property tax and pensions may all be on the table.

Uncertainty surrounding the budget and whether there will be a cut in the base rate will likely cause many buyers to hold off until the dust has settled, further adding to the market slowdown. Given that inflation is still running well above the BoE's target rate, we do not expect anything but the smallest of cuts, if at all.

Headlines

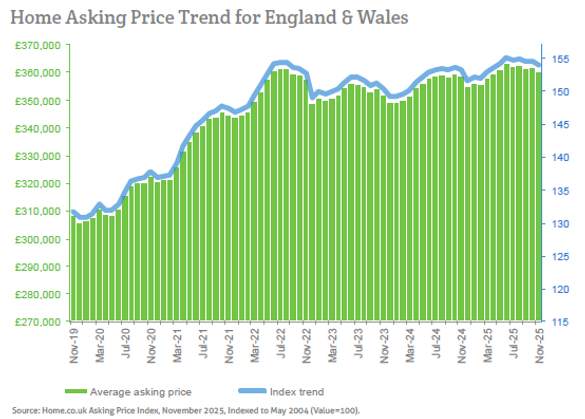

- The mix-adjusted average asking price for England and Wales dropped by 0.4% during October, bringing the annualised growth figure down to a mere 0.4%. Perhaps surprisingly, the North East and Yorkshire indicated the largest month-on-month declines.

- Annualised home price growth across England and Wales continues to be outpaced by monetary inflation. We estimate that overall real growth currently stands at around -4.2%. Even the best-performing regions are now suffering losses of capital value in real terms (vs. RPI ex-housing).

- There remains a veritable glut of unsold stock on the market. The total portfolio count for England and Wales is at its highest November reading since 2013. Oversupply is rebalancing the market in favour of buyers.

- Vendor numbers have swelled considerably. October showed the highest number of new instructions for that month in many years. Such a surge suggests that many investors are throwing in the towel. There were 7% more properties entering the market during October this year than in October 2024. The largest surges were in the East Midlands, Wales and the West Midlands (all up 11% year-on-year).

- Yorkshire remains the top regional property market growth leader with a year-on-year gain of 3.2%, albeit notably sub-inflation. Meanwhile, the South West remains the worst regional performer with a worsening annualised decline of 1.3%, just outpacing London's annualised decline of 0.9%.

- In the wake of a spectacular record-breaking summer, the sales market momentum is now plummeting. Notably, this greater throughput has not been sufficient to significantly reduce the unsold stock total. Typical Time on Market (TTM) for unsold properties is trending higher and is currently eight days more than in November last year.

- The annualised national growth in asking rents slides even further into the negative (now -3.7%). All English regions, Scotland and Wales indicate year-on-year falls in the mix-adjusted average asking rent. The worst performer is Wales with a decline of 11.6%.

- Seventeen of the 33 London boroughs indicate positive asking rent growth (up from 13 last month). Kensington and Chelsea is the slowest market (TTM: 37 days) while Waltham Forest is by far the speediest lettings borough (TTM: 12 days).

For media enquiries please contact: press@home.co.uk 0845 373 3580

For more information please visit.

Follow us on X.