15 Dec 2025

15 Dec 2025

The normal sales market dynamic has been grossly distorted by a late autumn budget and the Bank of England's pending decision on interest rates, says Home.co.uk's House Price Index for December.

Many potential vendors, fearful of yet another tax-grabbing budget, sat on their hands rather than enter the market, preferring to wait until the dust settles. The result of all this unnecessary uncertainty before the announcement on the 26th was that 29% fewer properties than expected entered the market in November.

The upshot of this dramatic reduction in supply is a steep fall in the number of properties on the market. In the near term this will support home prices which have been under heavy pressure recently due to a glut of unsold stock.

Seasonal expectations are such that agents' portfolios will shrink further before swelling with a surge in new listings during January.

Buyer demand in the New Year will depend in part on the next Bank of England (BoE) interest rate decision on 18th December. A cut of 0.25% is currently priced in by the markets and this move to lower borrowing costs would be a welcome early Christmas present for UK property sales. On the other hand, should the BoE be hawkish about inflation risks and hold the base rate at 4%, this would create significant negative sentiment among hopeful buyers.

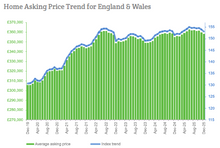

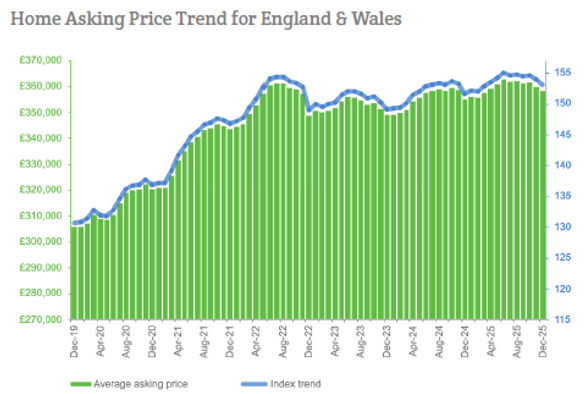

Home prices continue to slide as per seasonal expectations. During the last month prices fell in all English regions (except the South West where there was no change) and in Scotland. Only Wales recorded a small rise during November.

Headlines

- Vendor numbers crashed during November. Following the October surge which showed the highest number of new instructions for that month in many years, supply has slumped to the lowest November figure since the dark days of post-crisis 2010. Such a huge drop (29% down vs. Nov 2024) indicates the level of vendor hesitancy brought about by the controversial budget from Rachel Reeves and the forthcoming Bank of England decision on interest rates. The largest falls were in the South West, North West and Greater London.

- Home prices continue their seasonal slide. The mix-adjusted average asking price for England and Wales dropped by 0.5% during November, making the annualised growth figure just 1.0%, woefully outpaced by monetary inflation. Yorkshire indicated the largest month-on-month decline.

- The notable glut of unsold stock on the market that formed over the summer months is now reducing rapidly. Thanks in part to vendor hesitancy, the total portfolio count for England and Wales is now just 1.2% more than in December 2024. Total stock dropped by 40K during November and this large reduction will help to support prices while it lasts.

- The North West is the top regional property market growth leader with a year-on-year gain of 2.6%, followed by the West Midlands. Meanwhile, London remains the worst regional performer with an annualised decline of 0.7%.

- Typical Time on Market (TTM) for unsold properties continues to trend higher and is currently seven days more than in December last year.

- The annualised national growth in asking rents trends further into the negative (now -3.8%). Scotland, Wales and all English regions (apart from the North West which shows no change) indicate year-on-year declines in the mix-adjusted average asking rent. The worst performer is the East Midlands with an annualised decline of 13.4%.

- Twenty of the 33 London boroughs indicate positive asking rent growth (up from 17 last month). Kensington and Chelsea is the slowest market (TTM: 39 days) while Barking and Dagenham is the fastest lettings borough (TTM: 15 days).

For media enquiries please contact: press@home.co.uk 0845 373 3580

For more information please visit.