16 Aug 2014

16 Aug 2014

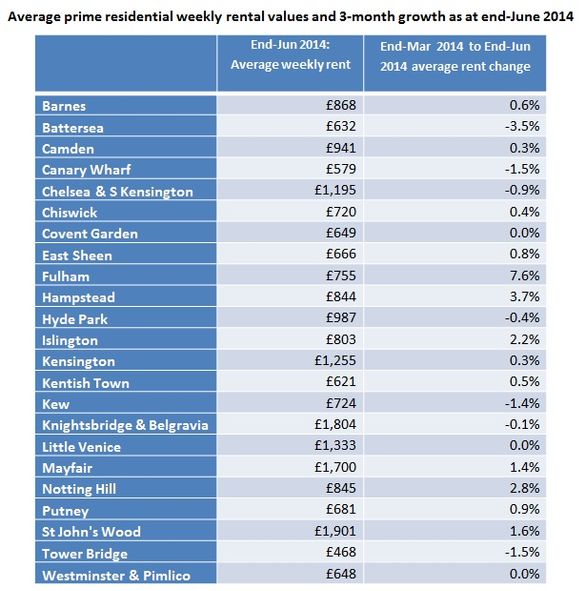

The slight shift in the supply/demand relationship resulted in the Chestertons Prime London Rental Values Index recording a decline in average rents of 0.8% in the 12 months ending in June 2014. However, the Index showed a modest increase in average rental values (+0.5%) in the second quarter compared to Q1. As usual, this masks variation between submarkets. The South West (-0.3%) was the only region to record a quarterly drop in prime rents while the North East (+0.9%) and Central (+0.9%) both saw rental growth over the quarter. At local market level, Fulham experienced the biggest rise in rents (+7.6%), due largely to strong demand for houses which were in very short supply, while Battersea suffered the sharpest decline (-3.5%).

The average weekly rent for the Index stood at £912 at the end of June. The highest average weekly rental values were achieved in St John's Wood (£1,901), Knightsbridge/Belgravia (£1,804) and Mayfair (£1,700). The lowest average weekly values were recorded in Canary Wharf (£579), Tower Bridge (£468) and Kentish Town (£621).

For the FULL report, contact André Kappelhoff at P1 Communications

Email: andre.kappelhoff@p1communications.com

Phone: 020 8614 7500

Outlook

With the economic recovery gathering momentum and simultaneously boosting the employment market, households are feeling more confident about property commitments. Recent survey evidence suggests that the majority of tenants would choose to own their property rather than rent, however with real incomes barely keeping pace with inflation and annual house prices in London rising by double digit percentages affordability is likely to make this an unobtainable dream for many. Average house prices in June in Kensington & Chelsea and Westminster, for example, were 57.5% and 54.4% respectively above their pre-global recession peak.

The tightening of mortgage lending criteria thanks to the implementation of the Mortgage Market Review, plus the likelihood that interest rates will rise before next year's General election and possibly before the end of this year, mean that many households will be forced into the private rented sector. The number of households in privately rented accommodation could rise by 131,250 between 2011 and 2021 even if the current ratio of 25% remains static. However, if the level of increase seen between 2001 and 2011 is maintained then this figure could rise to 492,630 or 34.5% of all households.

In the shorter term, with supply and demand becoming better aligned, rents are likely to continue to increase gradually across the board over the reminder of this year, aided by a likely rise in the number of “forced renters”. Increased activity from relocation agents also points to growing tenant demand from the corporate sector. The best prospects for growth lie in the decentralised areas where average rents are lower than in the prime central locations and will offer tenants better value for money.

In view of the above, we have revised our forecast for prime London rental growth for 2014 slightly upwards to 2.5% with a slight acceleration to 3% in 2015.